Whether you’re saving up to make a large purchase, or you just like to have a solid amount of emergency funds in case of any unexpected situations that life may decide to throw your way – a high-yield savings account can help you hit your savings goals faster and make extra funds available to you when you need them most. In February 2019, Citibank announced their newest high-yield savings account: Citi Accelerate. As of November 2022, the APY on the account is 3.10% APY with no limits on earnings and there is no minimum opening deposit required.

And, since this account is operating through online banking, Citibank doesn’t incur the same costs associated with brick-and-mortar bank establishments, so they are able to pass those savings on to you through higher APY and lower account fees.

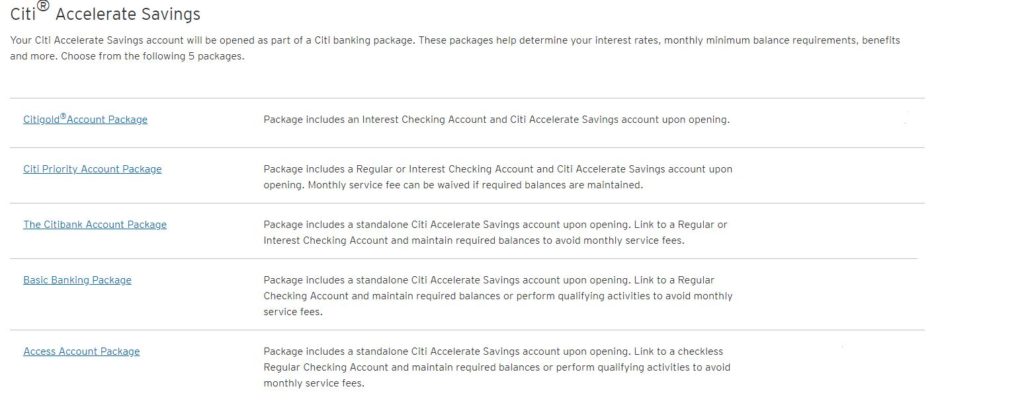

What is Citi Accelerate Savings?

Citi Accelerate is a high-yield savings account that must be opened as a part of one of Citibank’s current banking packages. The banking package that you choose will determine the rates you will receive on your savings.

Citi Accelerate Savings is currently available in: AL, AK, AZ, AR, CO, DE, GA, HI, ID, IN, IA, KS, KY, LA, OK, ME, MA, MI, MN, MO, MS, MT, NE, NH, NM, NC, ND, OH, OR, PA, RI, SC, SD, TN, TX, UT, VT, WA, WV, WI and WY and the following territories, possessions and military addresses of AA, AE, AP, AS, GU, MP, PR and VI.

Citi Accelerate Savings Account Fees

A Citi Accelerate Savings Account does have a monthly service fee of $4.50. But, if you maintain a minimum balance of $500 it can be waived.

A $2.50 ATM fee may apply if you use a non-Citibank ATM.

They also offer overdraft protection of $10 per overdraft transfer. You must opt-in to their “Safety Check” contributing account feature.

*Overdraft fees are waived for their Citigold® Accounts, Citi Priority Accounts and Access Accounts. You can also avoid Overdrafts and Overdraft Protection Transfer Fees if you transfer funds online, by phone or ATM.

What Are The Benefits Of A Citi Accelerate Savings Account?

- No minimum opening deposit required

- APY of 3.10%

- 24/7 online access to you accounts

- No early termination fee

- Free ID theft protection through Citi Identity Theft Solutions

- Free online & mobile fraud protection

- Earning Citi ThankYou Reward Points

- The ability to set up automatic transfers to help your savings grow

- The option to sign up for overdraft protection through their “Safety Check” program

- The option to set up alerts for free updates on your accounts

What Are The Disadvantages Of A Citi Accelerate Account?

- You must maintain a monthly balance of at least $500 to avoid the monthly service fee

- It must be linked to a Citibank Account Package

- Limit of 6 outgoing transfers/withdrawals per month (per federal regulations)

- The Citi Accelerate Savings Account does not offer check writing

Additionally, while 3.10% APY is especially high-yield by today’s standards, it’s actually not the highest APY out there.

As of November 2022, here are some rates from competitors that you may want to check out:

- Aspiration Bank – 3.00% APY

- TAB Bank – 3.00% APY

- Citi Accelerate – 3.10% APY

- First Foundation Bank Online Savings – 3.60% APY

- Barclays Bank – 3.00% APY

- CIBC Bank – 3.27% APY

- Goldman Sachs – Marcus Account – 3.00% APY

- Synchrony Bank – 3.00% APY

- TIAA Bank – 0.80% APY

- Ally Bank – 0.75% APY

- Citizens Access – 0.75% APY

- Capital One 360 Performance Savings – 0.70% APY

- Discover – 0.70% APY

- American Express Personal Savings – 0.65% APY

- CIT Bank Savings Builder – 3.25% APY

- MySavingsDirect – 0.50% APY

- Vio Bank – 0.50% APY

- HSBC Direct – 0.05% APY

Is Citi Accelerate Insured by the FDIC?

Yes. Citibank is a FDIC member. This means that funds deposited in a Citi Accelerate Savings Account are insured up to the maximum allowed by law.

The Federal Deposit Insurance Corporation (FDIC) is a United States government corporation providing deposit insurance to depositors in U.S. commercial banks and savings institutions. The FDIC insures deposits according to ownership category (such as individual, joint or accounts with beneficiaries). The current maximum amount is $250,000 per depositor, per insured bank, for each account ownership category.

How Do You Open A Citi Accelerate Savings Account?

It should take about 10 minutes to open your account online. All you need is access to your personal details (name and contact information) in addition to your Social Security number and a valid ID. In other words, it’s fairly easy!

You can apply online for an account here.

How To Access Your Citi Accelerate Savings Account

Online: You can access your online savings account at https://online.citi.com. Log in with your user ID and password.

Mobile Device: You can download the Citi App for your mobile device.

Chat: You can communicate directly with a Customer Service Representative via the Chat button which appears when you are logged in to online.citi.com. The green icon next to “Live Chat” indicates that Chat is live. Red icon indicates ‘live chat’ is not currently available.

Automated Phone 24/7: Citibank provides an automated phone system at 1-800-374-9700 (TTY: 1-877-693-0372) that allows you to check your balance, transfer funds and more.

Live Representative: You can also speak with a live representative at 1-800-374-9700 (TTY: 1-877-693-0372).

For current interest rates and Annual Percentage Yields: You can visit citibank.com or call CitiPhone Banking at 1-833-418-6393.

Outside of the United States: Internationally, you can call 1-813-604-3000 for general support and servicing.

Bottom Line

In conclusion, it takes time to build up money in a savings account, but opening the Accelerate high-yield savings with a trusted name like Citibank should help you reach your savings goals faster with their automatic transfer feature and competitive 3.10% APY.

And of course, before signing up for a bank account, you’ll want to read the fine print, which can be found here: Citi Client Manual – Consumer Accounts. As of June 2020, Citibank has implemented important changes to their daily and weekly transfer limits on some of their account packages.

Banking Health Score

There are many banks and financial institutions to choose from and it is important to be able to distinguish the good from the bad. Our team reviews each bank on a monthly basis to ensure that the information we share is as up to date as possible. Not only is the financial strength of a company important, but also how well their customer service is rated by actual customers like you.

We also believe that in order to determine how well a bank is functioning, that several sources should be utilized to compare one bank to another.

That said, here is a list of scores from trusted sources that you should consider before making your banking decisions.

Citibank- Bank Health Scores

Bank Professor’s Bank Score = ⭐⭐⭐⭐ 4 stars out of 5 stars

Additional Scores

- Bankrate’s Safe and Sound Rating: 4.1 out of 5 stars

- BauerFinancial Star Rating: 4 out of 5 stars

- BankTracker Troubled Asset Ratio: 3.78

- FDIC: Actively insured

More about the rating system:

- BankProfessor rates banks monthly on a one-to-five scale based on revenue, net income, total assets, total equity, capital ratio, customer reviews, rating agency scores, profitability, and troubled asset ratio.

- Bankrate.com ranks banks and credit unions quarterly on a one- to five-star system, with one being the lowest rating and five the highest. The rating is given based on regulatory filings about the financial institution’s capital adequacy, asset quality, profitability and level of cash available. It compares those levels with peer and industry norms.

- BauerFinancial offers a similar star rating system as Bankrate (a one- to five-star system, with one being the lowest rating and five the highest).

- BankTracker was created by the Investigative Reporting Workshop of American University and MSNBC.com. They determine a bank’s troubled asset ratio. According to the site, the ratio is “a strong indicator of severe stress inside a bank because it shows the bank’s ability to withstand loan losses”. In other words, the higher the ratio, the more “trouble” they are in.

How to Close An Account with Citibank

If you wish to close your online account with Citibank, you will first need to make sure that all pending transactions have cleared before you start transferring any money out of the account. Then, you can contact the bank at 1-800-374-9700 or send correspondence via mail to Citibank PO Box 6500 Sioux Falls, SD 57117 to request account closure.

You can also login to your account online and send a secure message to Citibank’s customer service department to request account closure.

Typically account closure requests will need to be made in writing (even if you call first) using their Account Closure Form. When you speak with a customer service representative, make sure to ask if they prefer written requests to be received via standard mail, e-mail or fax.

Once the form is received, you should receive a response or confirmation of account closure within a few business days.

History

Citibank is a branch of Citigroup which provides lines of credit and loans to consumers. Founded on June 16, 1812 in New York City, USA, Citibank has typically been above the curve in terms of advancement of their products and was one of the only U.S. banks in the 1970’s to offer their members 24/7 access to their bank account via ATMs. By the early 1980’s, they were also one of the first banks to pioneer online banking for their members via dial-up. And in 1994, Citibank became the world’s largest card issuer. Since that time, Citibank has seen steady expansion and has continued to make improvements to their offerings to ultimately maintain a user-friendly and practical product line for their customers.

Kate’s career has focused on consumer behavior and marketing analysis. She is a Senior Staff Writer for BankProfessor.com.