Looking into opening a CIT Savings Builder account?

Online savings accounts are a rapidly growing trend that help people save money faster and smarter. Arguably, some of the greatest features of online accounts include ease of access, higher interest rates as well as the ability to set up notifications and automatic transfers.

Needless to say, the competition of online banking is fierce – with banks always trying to be a cut above their rivals by offering rates that consumers can’t refuse. Right now, CIT Bank’s “Savings Builder” account has one of the highest APYs in the market.

CIT Bank (member FDIC) is a completely online bank that is redefining banking in the digital age by offering a 0.55% APY on their Savings Builder accounts.

What is A CIT Savings Builder Account?

The CIT Savings Builder is an online, high-yield savings account with no monthly maintenance fees or transfer fees. Furthermore, the minimum deposit to open an account is only $100, and from there – CIT Savings Builder makes it easy to obtain up to 0.55% interest annually, by giving members 2 ways to earn it:

You need to either…

- Maintain an account balance of $25,000 or more per month. OR

- Open an account with as little as $100, and then deposit at least $100 each month.

The CIT Savings Builder also operates on a “Tiered System” for their APY as follows:

| Interest tier | Balance requirement | APY |

|---|---|---|

| Base | Less than $25,000 | 0.31% |

| Upper | Less than $25,000 with monthly deposits of at least $100 | 0.55% |

| Upper | More than $25,000 | 0.55% |

You can deposit money at any time into your account through ACH transfer, incoming wire or by mailing a check to CIT Bank.

Funds in a Savings Builder account can be accessed at any time if you need to withdraw the money. For instance, withdrawals can be made via wire, outgoing ACH transfer or CIT can mail you a paper-check.

What Are The Account Fees For A CIT Savings Builder Account?

While there are no maintenance or minimum balance fees, there are fees associated with certain activities in a CIT Savings Builder account.

Here is the current fee schedule for CIT Savings Builder Accounts:

| Activity | CIT Bank Fee |

|---|---|

| Account Closure | Free |

| Mail Check | Free |

| Monthly Service Fee | Free |

| Online Transfer | Free |

| Incoming Wire Transfer | Free |

| Outgoing wire transfer for accounts with an average daily balance of $25,000 or more | Free |

| Outgoing wire transfer for accounts with an average daily balance of less than $25,000 | $10 per wire transfer |

What Are The Benefits Of A CIT Savings Builder Account?

In this section, we’ll outline what current customers have said are the advantages of their CIT savings builder account.

- Higher than average APY

- FDIC-Insured

- No annual or monthly maintenance fees

- No minimum balance fees

- Free (or low costing) wire transfers

- User-friendly mobile app and online experience

- Daily compounding interest

Although 0.55% APY is a great rate in today’s world, there are some competitors out there with higher APY or some banks that may have better perks.

As of November 2022, here are some rates from competitors that you may want to check out:

- Aspiration Bank – 3.00% APY

- TAB Bank – 3.00% APY

- Citi Accelerate – 3.10% APY

- First Foundation Bank Online Savings – 3.60% APY

- Barclays Bank – 3.00% APY

- CIBC Bank – 3.27% APY

- Goldman Sachs – Marcus Account – 3.00% APY

- Synchrony Bank – 3.00% APY

- TIAA Bank – 0.80% APY

- Ally Bank – 0.75% APY

- Citizens Access – 0.75% APY

- Capital One 360 Performance Savings – 0.70% APY

- Discover – 0.70% APY

- American Express Personal Savings – 0.65% APY

- CIT Bank Savings Builder – 3.25% APY

- MySavingsDirect – 0.50% APY

- Vio Bank – 0.50% APY

- HSBC Direct – 0.05% APY

What Are The Disadvantages Of A CIT Savings Builder Account?

- You have to have at least $25,000 in savings or commit to saving $100 each month to get the 0.55% APY

- CIT Savings Builder is online-only. There aren’t any brick-and mortar locations that you can visit in person

- Base tier interest rate is less competitive

- Limited to 6 withdrawals per month. If you go over 6 in a month, you’ll be charged $10 per withdrawal

- No ATM card

- Limited customer service hours

- Frequent mobile app crashes have been reported by users

Is A CIT Savings Builder Account Right For You?

A CIT Savings Builder Account may be right for you if:

- Firstly, You want your money in a savings account that can be accessed by you at any time (liquidity)

- FDIC protection is important to you

- You can afford to keep a $25,000 balance or make at least one deposit of $100 per month

- ATM access to your money is not necessarily important to you

- You don’t need or want access to physical branch locations / in-person support

Is A CIT Savings Builder Account FDIC-Insured?

Yes. CIT Bank, N.A. is a FDIC member. Therefore, any funds deposited in a CIT Savings Builder Account are insured up to the maximum allowed by law.

The Federal Deposit Insurance Corporation (FDIC) is a United States government corporation providing deposit insurance to depositors in U.S. commercial banks and savings institutions. The FDIC insures deposits according to ownership category (such as individual, joint or accounts with beneficiaries). The current maximum amount is $250,000 per depositor, per insured bank, for each account ownership category.

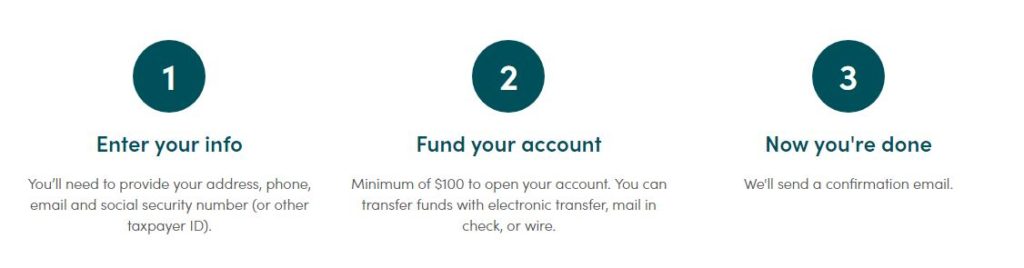

How Do You Open A CIT Savings Builder Account?

The application process for a CIT Savings Builder account usually takes the average member 5-10 minutes to complete the application online. In other words, it’s a fairly quick and simple process.

First, visit https://www.cit.com/

Next, click “Open an account” to be redirected to the Account Application

Then, fill out your personal details (You’ll need to provide your address, phone, email and social security number, or other taxpayer ID).

Finally, fund your account with at least $100 minimum deposit.

That’s it! Once your account is active, you can log on any time 24/ 7 to deposit and withdraw funds or make changes. You can also set up automatic deposits into your account to effortlessly build your savings.

How To Access Your Savings Builder Account:

Online: Access your account by logging in with your username and password on: www.CIT.com

Mobile Device: Bank on your phone/tablet through their mobile app.

Call: 855-462-2652 (within U.S.) ; 626-535-8964 (outside U.S.)

Fax: 866-914-1578

Hours

Monday through Friday: 8:00 a.m. — 9:00 p.m. (ET)

Saturday: 9:00 a.m. — 5:00 p.m. (ET)

Sunday: 11:00 a.m. — 4:00 p.m. (ET)

Mailing Address

CIT Bank, N.A.

75 North Fair Oaks Ave

Pasadena, CA 91103

Bottom Line

In conclusion, whether you’re putting money away for a down payment, a family vacation, or to hold onto for a rainy day, having savings in the bank is important. But to be getting one of the highest APYs in the market on your savings is an added bonus that makes the saving you’re already doing even better. Furthermore, the CIT Savings Builder offers an interest rate that is well-above the national average, while encouraging you to continue to save every month. So – if you have more than $25,000 in savings, or can commit (at least) to adding $100 to your account each month, you’ll earn market-topping interest on your funds.

History

CIT Bank was founded in 1908 by Henry Ittleson in St Louis, Missouri. The company withstood the pressures of the Great Depression and in addition, continued to see success through the post-war boom of the 1960s to through the technological innovations of the 1980s, 90s and 2000s. The retail banking division of CIT is currently headquartered in Pasadena, CA. CIT provides deposit accounts, certificates of deposit (CDs), money market accounts, home mortgages, and working capital loans to businesses.

CIT Bank consists of an online bank and its OneWest Bank division. According to their website – it was estimated in December 2018 that CIT had approximately $50 billion in assets.

Banking Health Score

There are many banks and financial institutions to choose from and it is important to be able to distinguish the good from the bad. Our team reviews each bank on a monthly basis to ensure that the information we share is as up to date as possible. Not only is the financial strength of a company important, but also how well their customer service is rated by actual customers like you.

We also believe that in order to determine how well a bank is functioning, that several sources should be utilized to compare one bank to another.

That said, here is a list of scores from trusted sources that you should consider before making your banking decisions.

CIT – Bank Health Scores

Bank Professor’s Bank Score = ⭐⭐⭐⭐ 4 out of 5 stars

Additional Banking Scores

Bankrate’s Safe and Sound Rating : 4.3 out of 5 stars

BauerFinancial Star Rating: 5 out of 5 stars

BankTracker Troubled Asset Ratio: 7.75

FDIC: Actively insured

More about the rating system:

• Bank Professor rates banks monthly on a one-to-five scale based on revenue, net income, total assets, total equity, capital ratio, rating agency scores, profitability, and troubled asset ratio.

• Bankrate.com ranks banks and credit unions quarterly on a one- to five-star system, with one being the lowest rating and five the highest. The rating is given based on regulatory filings about the financial institution’s capital adequacy, asset quality, profitability and level of cash available. It compares those levels with peer and industry norms.

• BauerFinancial offers a similar star rating system as Bankrate (a one- to five-star system, with one being the lowest rating and five the highest).

• BankTracker was created by the Investigative Reporting Workshop of American University and MSNBC.com. They determine a bank’s troubled asset ratio. According to the site, the ratio is “a strong indicator of severe stress inside a bank because it shows the bank’s ability to withstand loan losses”. In other words, the higher the ratio, the more “trouble” they are in.

How to Close An Account with CIT Bank

If you wish to close your account with CIT Bank, you will first need to make sure that all pending transactions have cleared before you start transferring any money out of the account. Then, you can contact the bank at 1-855-462-2652 or send correspondence via mail to CIT Bank at P.O. Box 7056 Pasadena, CA 91109-9699 to request account closure.

You can also login to your account online and send a secure message to CIT’s customer service department to request account closure.

Typically account closure requests will need to be made in writing (even if you call first). When you speak with a customer service representative, make sure to ask if they prefer written requests to be received via standard mail, e-mail or fax.

You should receive a response or confirmation of account closure within a few business days.

Kate’s career has focused on consumer behavior and marketing analysis. She is a Senior Staff Writer for BankProfessor.com.